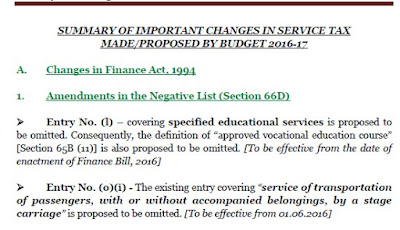

A. Changes in Finance Act, 1994

1. Amendments in the Negative List (Section 66D)

- Entry No. (l) – covering specified educational services is proposed to be omitted. Consequently, the definition of “approved vocational education course” [Section 65B (11)] is also proposed to be omitted. [To be effective from the date of enactment of Finance Bill, 2016]

Entry No. (o)(i) - The existing entry covering “service of transportation of passengers, with or without accompanied belongings, by a stage carriage” is proposed to be omitted. [To be effective from 01.06.2016]

- Entry No. (p)(ii) - The existing entry covering “services by way of transportation of goods by an aircraft or a vessel from a place outside India up to the customs station of clearance” is proposed to be omitted. [To be effective from 01.06.2016]

The domestic shipping lines registered in India will pay service tax under forward charge while the services availed from foreign shipping line by a business entity located in India will get taxed under reverse charge at the hands of the business entity. The service tax so paid will be available as credit with the Indian manufacturer or service provider availing such services (subject to fulfillment of the other existing conditions). It is clarified that service tax levied on such services shall not be part of value for custom duty purposes.

In addition, Cenvat credit of eligible inputs, capital goods and input services is being allowed for providing the service by way of transportation of goods by a vessel from the customs station of clearance in India to a place outside India.

Implication: Basically ocean freight with respect to import of goods into India has become liable to service tax. Although credit of service tax is made available to the manufacturers or service providers, in case of traders, it will add to their cost of purchase. Also, ocean freight is included in the assessable value for calculation of customs duty. Hence it will lead to double taxation of ocean freight.

Further, ocean freight in relation to export of goods out of India is no more an exempt service for the purpose of Cenvat Credit Rules. Accordingly, cenvat credit of duty paid on inputs or capital goods or service tax paid on input services have been made available to the shipping lines.

2. Other Amendments in Finance Act, 1994

[To be effective from the date of enactment of the Finance Bill, 2016]

- Lottery distributor or selling agent – The Explanation 2 to section 65B(44) of the Finance Act, 1994 has been proposed to be amended to clarify that “activity carried out by a lottery distributor or selling agents of the State Government under the provisions of the Lotteries (Regulation) Act, 1998 (17 of 1998)” is leviable to service tax.

- Declared Services (Section 66E) – A new entry “Assignment by the Government of the right to use the radio-frequency spectrum and subsequent transfers thereof” has been proposed to be declared as a service under section 66E of the Finance Act, 1994, so as to make it clear that assignment by Government of the right to use the spectrum as well as subsequent transfers of assignment of such right to use is a service leviable to service tax and not sale of intangible goods.

- Section 67A - Section 67A of the Finance Act, 1994 has been proposed to be amended to obtain specific rule making powers in respect of Point of Taxation Rules, 2011. [To be effective from 01.03.2016]

- Section 73 - The limitation period for recovery of service tax not levied or paid or short- levied or short paid or erroneously refunded, for cases not involving fraud, collusion, suppression etc. is proposed to be enhanced by one year, i.e., from 18 months to 30 months from the date of such non-levy/short levy/short paid/erroneous refund.

- Section 75 – Section 75 of the Finance Act, 1994 has been proposed to be amended to charge a higher rate of interest from a person who has collected any amount as service tax from the service recipient but has failed to pay the amount so collected to the credit of the Central Government on or before the date on which such payment becomes due. The new interest rates are given as below:

CLICK HERE / CLICK HERE TO DOWNLOAD FULL PDF EBOOK

Thanks to CA Narayan Kumar Agarwal

1. Amendments in the Negative List (Section 66D)

- Entry No. (l) – covering specified educational services is proposed to be omitted. Consequently, the definition of “approved vocational education course” [Section 65B (11)] is also proposed to be omitted. [To be effective from the date of enactment of Finance Bill, 2016]

Entry No. (o)(i) - The existing entry covering “service of transportation of passengers, with or without accompanied belongings, by a stage carriage” is proposed to be omitted. [To be effective from 01.06.2016]

- Entry No. (p)(ii) - The existing entry covering “services by way of transportation of goods by an aircraft or a vessel from a place outside India up to the customs station of clearance” is proposed to be omitted. [To be effective from 01.06.2016]

The domestic shipping lines registered in India will pay service tax under forward charge while the services availed from foreign shipping line by a business entity located in India will get taxed under reverse charge at the hands of the business entity. The service tax so paid will be available as credit with the Indian manufacturer or service provider availing such services (subject to fulfillment of the other existing conditions). It is clarified that service tax levied on such services shall not be part of value for custom duty purposes.

In addition, Cenvat credit of eligible inputs, capital goods and input services is being allowed for providing the service by way of transportation of goods by a vessel from the customs station of clearance in India to a place outside India.

Implication: Basically ocean freight with respect to import of goods into India has become liable to service tax. Although credit of service tax is made available to the manufacturers or service providers, in case of traders, it will add to their cost of purchase. Also, ocean freight is included in the assessable value for calculation of customs duty. Hence it will lead to double taxation of ocean freight.

Further, ocean freight in relation to export of goods out of India is no more an exempt service for the purpose of Cenvat Credit Rules. Accordingly, cenvat credit of duty paid on inputs or capital goods or service tax paid on input services have been made available to the shipping lines.

2. Other Amendments in Finance Act, 1994

[To be effective from the date of enactment of the Finance Bill, 2016]

- Lottery distributor or selling agent – The Explanation 2 to section 65B(44) of the Finance Act, 1994 has been proposed to be amended to clarify that “activity carried out by a lottery distributor or selling agents of the State Government under the provisions of the Lotteries (Regulation) Act, 1998 (17 of 1998)” is leviable to service tax.

- Declared Services (Section 66E) – A new entry “Assignment by the Government of the right to use the radio-frequency spectrum and subsequent transfers thereof” has been proposed to be declared as a service under section 66E of the Finance Act, 1994, so as to make it clear that assignment by Government of the right to use the spectrum as well as subsequent transfers of assignment of such right to use is a service leviable to service tax and not sale of intangible goods.

- Section 67A - Section 67A of the Finance Act, 1994 has been proposed to be amended to obtain specific rule making powers in respect of Point of Taxation Rules, 2011. [To be effective from 01.03.2016]

- Section 73 - The limitation period for recovery of service tax not levied or paid or short- levied or short paid or erroneously refunded, for cases not involving fraud, collusion, suppression etc. is proposed to be enhanced by one year, i.e., from 18 months to 30 months from the date of such non-levy/short levy/short paid/erroneous refund.

- Section 75 – Section 75 of the Finance Act, 1994 has been proposed to be amended to charge a higher rate of interest from a person who has collected any amount as service tax from the service recipient but has failed to pay the amount so collected to the credit of the Central Government on or before the date on which such payment becomes due. The new interest rates are given as below:

CLICK HERE / CLICK HERE TO DOWNLOAD FULL PDF EBOOK

Thanks to CA Narayan Kumar Agarwal

0 comments :

Post a Comment