Rule 6 of CCR, 2004 (As amended by FA, 2016)

• This rule does not apply. CENVAT credit can be claimed normally Case 1 – If Manufacturer/ Service Provider only produces/ provides taxable goods/ services.

• This Rule applies. Effectively, no CENVAT credit can be claimed at all Case 2 – If Manufacturer/ Service Provider only produces/ provides exempted goods/ services

• One of the two Options as described below must be exercised Case 3 – If Manufacturer produces both exempted and non-exempted goods/ Service Provider provides both exempted and nonexempted services

1. This amended provision will come into force from the 1st of April 2016. (But there is an

option for assessees to exercise this option for the FY 2015-16 too, as specified in clause

3AB of Rule 6)

2. Once any one of the two options has been exercised, it shall be applicable to all goods

produced/ services provided and cannot be withdrawn for the remaining part of the

Financial Year.

3. If the amounts are not paid within the prescribed time-limits, then interest @ 15% per

annum will be applicable.

Note 2: Comparing new rule with the previous rule-

In the old rule (which is technically the current rule when I am writing this), there were three

options –

i. Maintaining separate books of accounts

ii. Paying a specified %tage of the exempted turnover (Same as option 1 of new rule)

iii. Determining amount payable using some formulas

After reading both the rules, we realize that Option 2 of the new rule is nothing but a

combination of Option1 and Option 3 of the old rule.

Note 3: If 2nd option has been exercised, then following formalities must be

done-

I. The Assessee must INTIMATE to the SUPERINTENDENT-

1. Name, Address and registration number

2. Date from which the option has been exercised/ is proposed to be exercised

3. Description ofa.

Inputs/ Input Services used exclusively for manufacturing exempt goods or

providing exempt services

b. Such exempt goods and services

c. Inputs/ Input Services used exclusively for manufacturing taxable goods or

providing taxable services

d. Such taxable goods and services

4. The amount of Cenvat credit lying in balance as on the date of exercising this option

II. The Assessee must INTIMATE to the SUPERINTENDENT, WITHIN 15 DAYS from the

date of final payment/ settlement, –

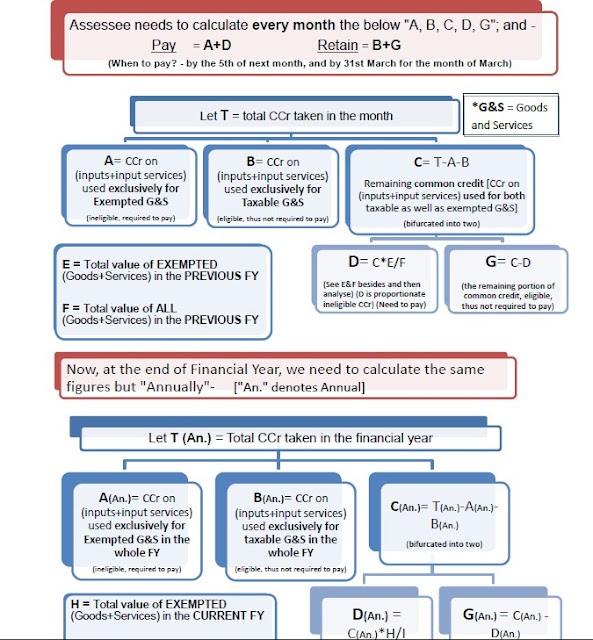

1. The monthly amounts A, B, D, G that had been calculated/ paid for the whole FY.

2. The annual amounts A(An.), B(An.), D(An.), G(An.) calculated for the FY.

3. The date and amount of final settlement, i.e., the “Differential amount” which was paid

or equivalent to which cenvat credit was taken.

4. Interest that is payable/ paid for late payment of the “final settlement amount”. (The

last date is 30th June)